The Oil industry and the Alberta economy are closely tied, and so, once the prices of Brent crude, WTI, and Alberta Heavy Oil fell, there was some worry about the future of the Albertan economy. But the question is, why did the price of oil fall so drastically, what is the price like now, and what does the future look like for oil?

The drop in the price of oil was a calculated move by OPEC, the Organization of the Petroleum Exporting Countries, which includes Algeria, Angola, Ecuador, Iran, Iraq, Kuwait, Libya, Nigeria, Qatar, United Arab Emirates, and Venezuela, with Saudi Arabia predominately at the helm of the ship, calling the shots. With these 12 countries producing half the world’s oil production and being home to more than 80% of the global oil reserves, the aim of OPEC is—usually—to co-ordinate policies that will stabilize the price and supply of oil. However, late last year, as a result of the global financial crises in 2008 lowering global demand, and a vastly increased output by US shale, OPEC, and more specifically, Saudi Arabia, decided not to cut their output, and this resulted in a plummet of global oil prices because of a combination of low demand and high output.

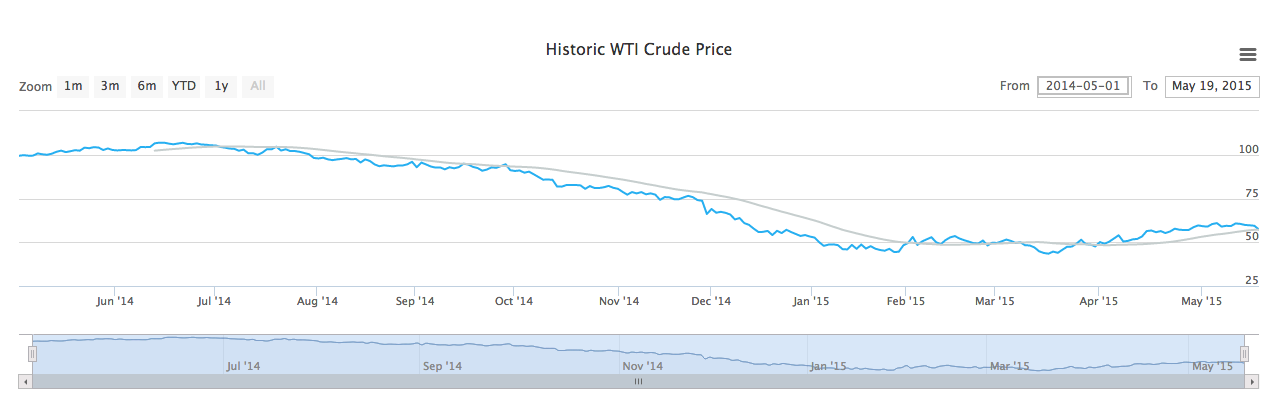

This drop in oil prices, from over $110 a barrel in June 2015, to less than half of that by the end of last year, was a calculated move by OPEC. The organization hoped to force oil operations elsewhere in the world, who have higher operating costs, like the shale oil producers in the United States and Alberta, to reduce their oil outputs. This intended goal has been relatively successful, with layoffs in North America reaching almost 100,000 people since crude prices began tumbling last year (http://www.wsj.com/articles/oil-layoffs-hit-100-000-and-counting-1429055740) and non-OPEC oil supply growing by just 680,000 barrels per day, down from a previous forecast of 850,000 barrels per day.

So where does that leave us now? Well, things aren’t as doom and gloom as people were making them out to be in the summer of 2014. As you can see from the graphic, the price of Oil is in a bit of a rebound phase. Global oil demands are expected to rise more than previously expected, with a forecast of 1.18 million barrels per day, beating the forecasted April estimate of 1.17 million. An Iranian senior energy official, Rokneddin Javadi, expects that oil prices will rise to $80, with or without the OPEC’s decision to cut oil production during its June meeting (http://oilprice.com/Energy/Oil-Prices/Oil-To-Return-To-80-With-Or-Without-OPEC-Cut-Says-Iranian-Official.html). (Sidenote: Iran was always for cutting oil production, but Saudi Arabia forced the issue) At the very least, prices are thought to stabilize in the near future, as Michael Wittner, global head of oil research at Societe General, said in a note released last week: “the simple fact of the matter is that the window for a correction will be closing in the coming few weeks.”

And while this all remains to be seen, we at Fox Oilfield are optimistic that prices will stabilize and operations in Alberta will normalize as a result.

If you would like to read more on the topic, here’s a few useful articles to get you started!

Alberta Oil Up Almost 80% Since March

Window For Oil Correction Closing

Global Oil Demand Expected To Rise: OPEC

Oil To Return To $80 With Or Without OPEC